The Pixelated Party Is Over for NFTs

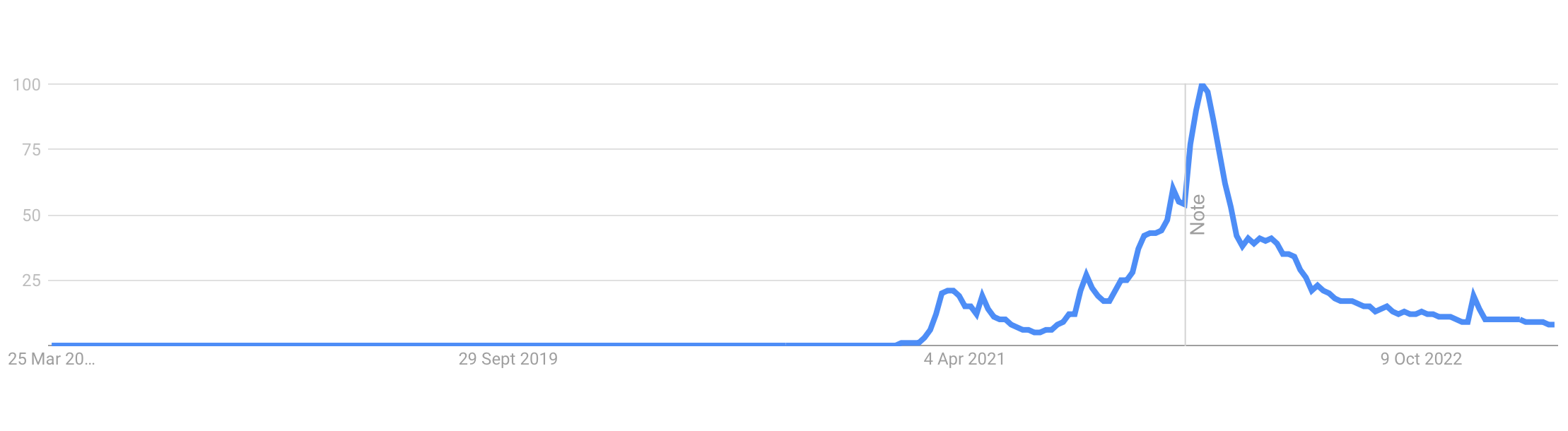

Last month, NFTs returned to the spotlight, seemingly regaining some of their former glory. Sales surged to $2 billion in February - numbers not seen since the Terra crash and a massive increase from the $117 million sales in January.

“We’re back baby,” rejoiced the JPEG monkey-holding diehards.

Unfortunately, the joy was short-lived. When we peel back the curtain on the data, it reveals this is no second coming for NFTs.

It was a washout.

Naughty Fake Trades

NFTs currently have two popular marketplaces; OpenSea and Blur. For the longest time, OpenSea ruled as the number one joint for buying and selling pixelated JPEGs. But, thanks to its new aggressive incentives program, Blur recently overtook OpenSea. On Feb 14, the platform launched its BLUR loyalty token, a reward designed to encourage users to refrain from selling their collections on other platforms (like OpenSea) and - this is important - to encourage lots of selling.

Blur also decided not to enforce royalties so long as the NFTs were not sold on a competitor's marketplace. Why? Again, to encourage lots of selling. (This is something of a turf war that’s kicked off between OpenSea and Blur, with both platforms only enforcing them if you sell your NFT between the two, rather than staying in each of their ecosystems. So much for “you’ll always get a share of the profit as the NFT continually gets flipped.” It was a nice concept while it lasted.)

Herein lies the problem. Blur is a platform for “pros,” meaning it’s aimed at those looking to flip their NFTs for profit. No diamond hands here. And with the platform now aggressively encouraging high-volume selling through its loyalty token and “optional” royalties, it resulted in a huge uptick in trading in February. The wholly predictable and should-have-seen-it-coming problem?

Most of it was wash trading.

Wash trading is driving up the price of NFTs by the buyer and seller (often the same person using different accounts). The buyer and seller sell the piece back and forth to drive up the cost but only publicly report the first sale, so other interested parties can’t easily tell it’s been swapped between the same wallets multiple times.

The practice was already rife, but with additional incentives now on offer, it’s clear that a few players on Blur went into overdrive. It turns out the majority of February’s volume was generated by a small number of whales who flipped their NFTs back and forth repeatedly to accumulate BLUR tokens. CryptoSlam, a platform that tracks NFT sales, announced that it was removing $577 million worth of Blur trades from its data because of “market manipulation.” Ultimately, it removed over $800 million of trades, nearly 80% of the total trades made between Feb 2-27. Wowzer.

According to Decrypt, ignoring these transactions means sales made on Blur in February were ~$6.47 million, a drop of 2% compared to January. That is a truer reflection of the NFT landscape and tracks better with figures from its rival OpenSea, which is expected to do around $325,000,000 in volume this month. Sizeable? Sure. But it’s not a touch on the $4 billion in NFT transactions OpenSea processed in January 2022, a high point from which it’s been downhill ever since.

In sum, February was a false boom for NFTs. There was no resurgence, just a combination of factors that led a few whales to get greedy, and the resulting feeding frenzy distorted the market numbers.

The reality is that the pixelated party has been over for some time.

Now Fully Toxic

The reason behind the downfall is obvious.

Nearly two years since they exploded into the mainstream, the technology still lacks real use cases.

Before anyone argues that two years is an acceptable bedding period, look at A.I. - it has already produced some pretty amazing use cases, several of which could be revolutionary. (Important note: much of it is a complete grift, just like the NFT space.) In the last six months, the technology has completely dwarfed the output of meaningful use cases achieved by NFTs over the last two years. The best thing NFTs have produced is Dookey Dash, a sewer-run game with bad poop jokes.

NFTs have been nothing but expensive status symbols that have made a handful of people filthy rich through either shrewd timing or the less-than-savory tactics of rug-pulling. The site Web3 is going great has been keeping count of the dollars stolen through scams — most of which are NFT projects promising to be the next Bored Apes — and the total stands at over $12 billion. As the market remains cold, many retail investors have discovered they’ve bought into a self-fulfilling ecosystem that’s stopped fulfilling itself. The evidence is mounting that many NFTs are sold between accounts held by the owner to pump up their price. Most projects rely solely on generating social media hype to launch with an inflated opening price before the first owners quickly sell and laugh their way to the digital bank. When they fail to do so, the project immediately crashes and leaves initial investors up shit creek without a paddle.

It hasn’t gone unnoticed. Rather than becoming widely adopted, the NFT brand has become toxic.

Like everything that becomes hazardous, nobody wants to be associated with it. And so, companies, brands and tech giants are dropping NFTs faster than they sold their souls to adopt them in the first place. The biggest name so far is Meta. The company once claimed NFTs would be integral to its Metaverse future; now, it’s completely winding down its work on NFTs.

Those who are pressing on are hoping a soft rebrand does the trick. Reddit launched “blockchain-backed Collectible Avatars.” Others prefer to use Digital Collectables. It’s a move as old as time. Whatever they want to call them, changing the buzzword a few times a year won’t solve the problem because the terminology isn’t the problem. The problem is that NFTs have no problem to solve and therefore lack any use cases that will spark wider public adoption.

Much like the laser eyes fad that plastered itself all over Twitter, NFTs are quickly vanishing from public view.

And much like the majority of the laser eye propagators who still push crypto to save face (and recover money), most people still pushing NFT technology don’t believe in it or the future it may one day bring to life. They just need the next person to come along who is drunk enough on KoolAid to buy it off them. (*cough* Ponzi scheme *cough*).

We can only hope those still ‘hodling’ their overpriced JPEG monkeys really did buy them to “appreciate the art.”

Because when it’s worth 99% less than when you bought it, what else do you have?